Ski-Doo vs. Polaris: The Battle for 130,000

Winter is one of the few industries left that cannot fake its supply chain. It either snows, or it doesn’t.

If you ride mountains, you understand that better than anyone. You plan trips around storms. You watch forecasts like markets. You commit to machines months before the first track touches powder.

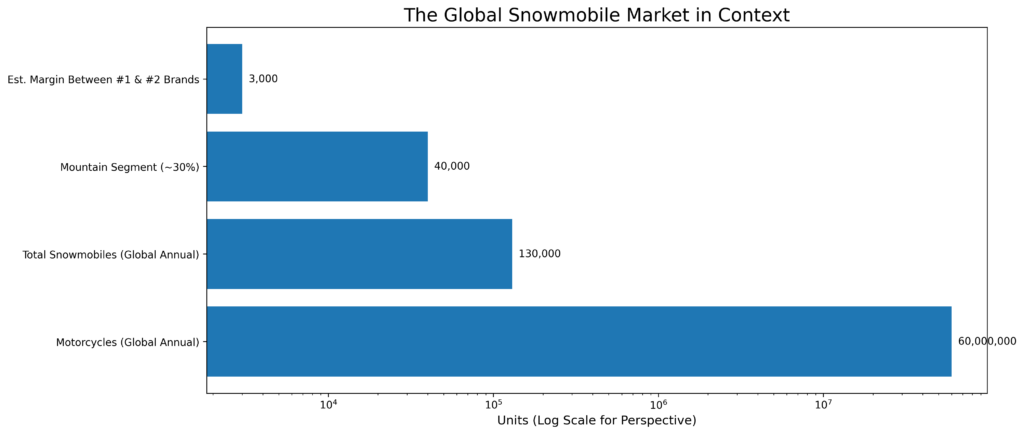

There are more than 60 million motorcycles sold globally each year, There are roughly 130,000 snowmobiles.

That comparison isn’t trivia – it’s perspective.

In a 60-million-unit industry, competition stretches wide, but in a 130,000-unit industry, competition tightens. And if you narrow that down to mountain sleds, you’re talking about roughly 40,000 units worldwide.

That’s the real arena.

Today, Polaris and Ski-Doo unveil their 2027 platforms on the same day. And in a market this small, especially in the mountain segment, that isn’t coincidence. It’s positioning.

The Pie Is Smaller Than It Looks

Snowmobiling isn’t just niche, it’s structurally constrained.

It is geographically concentrated in regions that receive reliable snowfall, seasonally dependent on a window that can stretch or shrink unpredictably, climate sensitive in ways few recreational industries are, and economically discretionary, relying almost entirely on consumers willing to invest in winter recreation rather than necessity.

And when we say 130,000 units globally, that number fractures quickly.

Based on typical market share estimates:

- BRP (Ski-Doo & Lynx) holds roughly 40–45%.

- Polaris holds approximately 35–40%.

- Arctic Cat accounts for around 10–15%.

- Yamaha and others divide what remains.

In actual units, that means:

- BRP moves roughly 52,000–58,000 sleds annually.

- Polaris moves roughly 45,000–52,000 annually.

- The remaining brands divide a much smaller slice.

The margin between first and second place is not millions of machines. It’s in the thousands.

And when you’re talking about mountain sleds, about 40,000 units worldwide, the difference can shrink even further. A 2-3% swing in mountain sleds can reshape perception for years.

Why the Same Day Matters to You

In larger global industries, companies stagger product releases to dominate the spotlight, stretching media cycles and controlling attention without interruption.

Snowmobiling doesn’t have that luxury.

The audience is finite, the season is finite, and the buying window is even more compressed. Most mountain riders aren’t making impulse purchases in December when the snow starts falling. They SnowCheck in spring. They commit before summer. They put deposits down months before the first storm ever touches the peaks.

When two dominant brands reveal on the same day, they compress your decision window and force immediate comparison.

This isn’t theatrical rivalry. It’s strategic compression.

The Mountain Multiplier

Mountain sleds disproportionately shape perception.

They carry higher MSRPs, stronger accessory attachment, and often define the identity of an entire brand.

For riders who spend their winters in deep snow, a sled isn’t just transportation, it’s an extension of who they are and how they ride. When a manufacturer establishes clear technological leadership through lighter chassis design, sharper ergonomics, improved driveline response, or refined suspension it does more than win spec-sheet comparisons.

It captures psychological ground.

And in a market measured in tens of thousands, perception shifts quickly into purchasing decisions.

The Dealer Reality

For dealers, reveal day isn’t about social media buzz, it’s about commitments.

Pre-season ordering programs, allocation forecasts, and floorplan financing aren’t abstract corporate strategies; they are balance-sheet decisions made by independent businesses betting on snowfall and rider confidence months before winter arrives. Much of that pressure crystallizes during SnowCheck, when the most committed buyers lock in their machines well ahead of the season.

What most riders don’t realize is that there is no public, industry-wide number for how many sleds are SnowChecked each year. Manufacturers do not disclose total presale volumes by segment, and there’s no public figure detailing how many mountain sleds were committed in spring versus sold off the floor in season. Those numbers exist internally. In a 40,000-unit mountain market, some of the most important numbers are effectively invisible.

So while riders debate horsepower and colorways, dealers are making six-figure allocation decisions without transparent benchmarks. They rely on local demand patterns, historical loyalty, snowfall forecasts, and instinct. In a cautious economy, reveal timing influences that instinct. If two brands drop on the same day, deposits shift in real time. Some riders commit early; others hesitate. And that hesitation matters.

The reveal calendar isn’t symbolic. It’s operational.

What This Moment Actually Represents

Within 24 hours, the spec sheets will circulate.

Specs and Comparisons dissected and debated in group chats and over on Alberta Sledderz.

But before the specifications dominate the conversation, consider the timing.

Two brands competing for slices of a 40,000-unit mountain segment, within a 130,000-unit global market, choosing to step into the same day.

In a 60-million-unit motorcycle world, that would feel dramatic.

In today’s economic climate where competition increasingly resembles survival – mountain snowmobiling feels like something else entirely: precise, calculated, and intentional.

The Real Question

When your segment is measured in tens of thousands…

When your buyers commit months before winter…

When perception shapes deposits…

How aggressively do you defend your ground?

The 2027 Platforms Go Live Today

2027 Polaris Reveal

2027 Lynx Reveal

2027 Ski-Doo Reveal

**Full technical breakdowns will publish as embargoes lift.